.jpg)

Deferred retirement occurs when a worker continues working despite having already met all the requirements for retirement. This entitles them to what is known as the "deferral supplement".

DEFERRAL SUPPLEMENT

Requirements:

- Retirement at an age above the applicable standard retirement age.

- Minimum contribution period of 15 years.

- The deferral of retirement must occur because the worker remains active in the Social Security system, that is, they are still working.

How do you obtain the deferral supplement?

Albert Perez, employment lawyer

Ways to receive the supplement:

There are 3 options:

- A 4% increase in the pension for each year deferred, so if you defer retirement by 3 years, a 12% increase will be applied. This supplement can push the payment above the maximum pension cap, meaning it is possible to receive more than the statutory maximum. However, for those whose pension would exceed the legal cap, the increase is calculated against the maximum pension cap rather than the regulatory base. For example, if the regulatory base is €5,000, the 4% would not be applied to that figure but to €3,086, the current maximum cap. Using this deferral percentage, the maximum retirement pension obtainable is €3,853.28, regardless of how many years have been deferred.

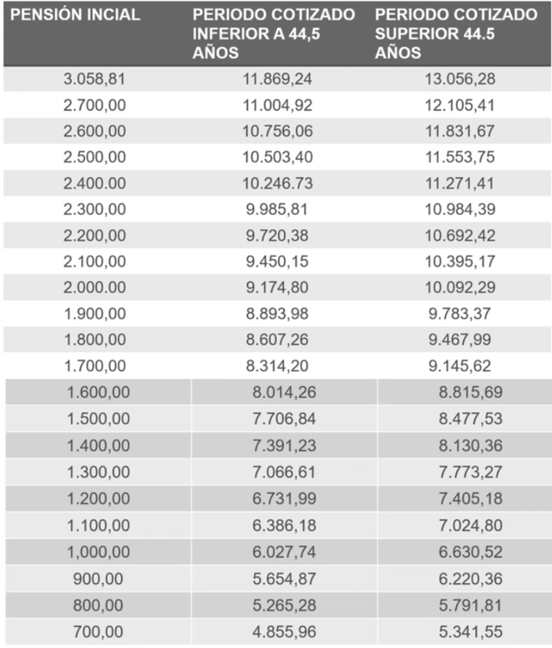

- Lump-sum payment: you receive a one-off lump sum calculated on the basis of your regulatory base and the number of years by which you have deferred your retirement.

The table below shows the lump-sum amount you would receive:

- Mixed option, percentage increase plus lump sum: this option has an additional requirement that the individual must have deferred retirement by at least 2 years.

- How does it work? The total period of deferral is split in two: one half attracts the percentage increase, while the other half is paid as a lump sum. For example, if 4 years have passed since the individual first became eligible to retire, they will receive an additional 8% percentage increase (equivalent to half the deferred period, i.e. 2 years), and the remaining 2 years will be paid as a lump sum based on their regulatory base, in accordance with the table above.

When and how can you choose how to receive the deferral supplement?

The payment method for deferred retirement is selected at the time of application. If no choice is made, the first option will apply by default, that is, the percentage increase based on the number of years of deferral.

Incompatibility with active retirement

Active retirement is not compatible with the deferral supplement.

If you opt for the percentage payment method, receipt of the supplement is suspended for the duration of any active retirement period.

If you opt for the lump-sum payment and have already received it, you will no longer be able to access active retirement.

Read more about active retirement

If you need assistance with your retirement, Conesa Legal offers a personalised service and we would be delighted to help: