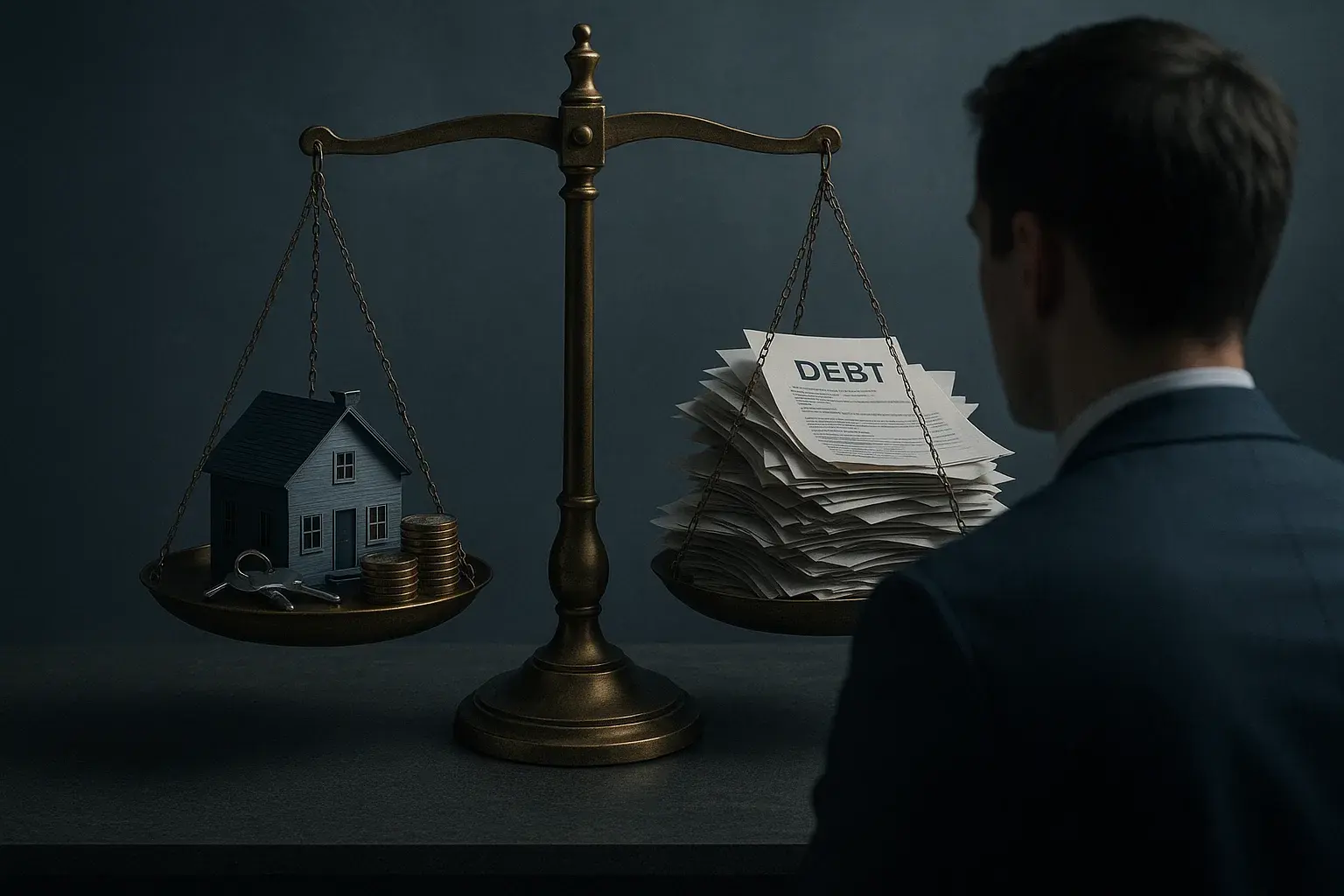

When faced with an estate with debts, it is natural to ask: "Do I also inherit the deceased's debts?" or "What happens if the estate's debts exceed its assets?" This scenario, while unfortunate, is more common than it might seem and can place heirs in a very difficult position. Under Spanish succession law, and particularly in Catalonia, which has its own rules in this area, there are legal mechanisms to deal with estates where liabilities exceed assets.

.png?width=123&height=123&name=Foto%20Maria%20Serra-modified%20(2).png)

Do heirs inherit the deceased's debts?

If the deceased owed money (a mortgage, loans, credit card balances, etc.), their creditors may seek payment from the heirs, but only if the heirs accept the inheritance. If the estate's debts exceed the value of the inherited assets, heirs could find themselves personally liable for the shortfall if they fail to take the appropriate precautions. Imagine inheriting a property worth €100,000, only to discover that the deceased left behind €150,000 in debts: accepting that inheritance without first investigating would mean taking on €50,000 of net debt out of your own pocket. This is why it is essential to understand the legal options available to you as an heir in order to protect your personal finances.

Options available to an heir when an estate carries debts:

When you are due to inherit an estate burdened with debts, you essentially have three legal options:

- - accept it outright and unconditionally,

- - accept it with benefit of inventory, or

- - renounce the inheritance. Let us look at what each option involves, along with its risks and benefits, particularly within the Catalan legal context. Outright acceptance (accepting the inheritance "as is").

1. Outright and unconditional acceptance

This is the traditional way of accepting an inheritance, whereby the heir takes on both the assets and the debts of the deceased. If you choose this route, your personal estate merges with that of the deceased: this means you will be liable for the debts of the inheritance even beyond the value of the assets inherited. In other words, if the debts exceed the value of the estate, you will have to cover the shortfall from your own funds.

- When might this be appropriate? Outright acceptance is only advisable if you are certain that the assets outweigh the liabilities (i.e., that there are more assets than debts), or if the debts are manageable and you wish to expedite the probate process.

- Main risk: If, after accepting, hidden debts come to light or you underestimated the liabilities, you could be legally required to cover them from your own estate. There is no going back: outright acceptance is irrevocable (except in exceptional cases involving a defect of consent).

Practical example: Juan accepts his uncle's estate without looking into the debts. He inherits a car and some savings (valued at €20,000), but unpaid loans of €50,000 subsequently come to light. Having accepted unconditionally, Juan must pay the €30,000 difference, even if it means drawing on his own savings. Had Juan done more due diligence or consulted a lawyer, he might well have chosen a different option. 2.- Acceptance with benefit of inventory (accepting only if there are net assets).

2. Acceptance with benefit of inventory

This is the most valuable legal tool available to an heir who suspects there may be significant debts. By accepting with benefit of inventory, you limit your liability for inherited debts to the value of the assets you inherit. This means you will not be required to pay the estate's debts beyond what the inherited estate itself covers; your personal assets remain protected against those excess liabilities. In practical terms, accepting with benefit of inventory is equivalent to saying: "If the estate has debts, they will be paid solely from what the estate contains; if that is not enough, the creditors will absorb the shortfall, and I will not contribute a penny of my own money."

To take advantage of this protection, the law requires you to draw up a detailed inventory of the estate. Hence the name: you take stock of all assets and all debts before deciding how to proceed. Bear the following points in mind:

- Deadlines: In Catalonia, the heir has a statutory period of 6 months from the moment they become aware they have been called to the inheritance to formalise the inventory. This is a reasonable timeframe in which to gather information from banks, consult the Land Registry, and review the deceased's documents, etc. Important: If you allow this deadline to pass without taking any action and subsequently attempt to invoke the benefit of inventory, you may lose that right and be treated as an unconditional acceptor.

- Formalisation: The inventory must be drawn up before a notary. In Catalonia, an inventory prepared as a private document is also accepted provided it is subsequently submitted to the tax authorities (for example, to settle inheritance tax), but the safest approach is to execute it by means of a notarised public deed. The inventory must list all assets, rights, debts, and liabilities forming part of the deceased's estate, together with their value or amount.

- Effects of accepting with benefit of inventory: Once you have accepted on this basis, you will only pay the deceased's creditors out of the inherited assets, never out of your own personal assets. If, after liquidating all the estate's assets, debts still remain unpaid, those creditors will have no recourse against you personally (they will bear the loss). Furthermore, any claim you may have had as an heir against the deceased will be preserved intact (for example, if the deceased owed you money for any reason), since the two estates are not merged.

3. Renunciation of the inheritance (disclaiming the inheritance)

The third option is simply not to accept the inheritance, which in legal terms is known as disclaiming or renouncing the inheritance. Renouncing means that you reject both the assets and the debts of the deceased, with the effect that you are treated as though you were never an heir. It is a drastic decision, but sometimes a very sensible one: if it is clear that the estate is heavily indebted and holds nothing of value to you, renouncing may be the most prudent course of action to avoid being dragged into the deceased's obligations.

Key points regarding renunciation:

- Form: Renunciation must be made expressly and in a public document (normally before a notary, by means of a deed of renunciation of inheritance). Simply "doing nothing" is not sufficient; the proper course is to formalise the renunciation correctly.

- Effects: If you renounce, you receive nothing from the estate, but you are also not liable for its debts. You are legally deemed never to have been an heir. The inheritance will then pass to the next entitled persons (for example, if you renounce your father's inheritance, your children may step into your place if the law so provides, or it may pass to your siblings, and so on, depending on the applicable order of succession). If all those entitled renounce, the estate will be declared yacente (an estate in abeyance, with no active heir) and may ultimately be allocated to the Spanish State or to the Generalitat de Catalunya as the last resort, after paying creditors as far as the existing assets allow.

- Inheritance tax: One practical point worth noting is that if you renounce the inheritance purely and unconditionally (without receiving anything in return), you will not be liable for inheritance tax on assets you are not inheriting. However, the renunciation must be made before taking possession of any assets, and without undue delay, in order to be considered valid for tax purposes and not treated as a transfer to a third party.

Are there any downsides to renouncing? The main drawback is obvious: you also lose any assets that may form part of the estate. Sometimes, even where debts exist, it may be worth accepting the inheritance if there is a sentimental or valuable asset you wish to keep and the debts are manageable. For this reason, the decision should only be made after a careful review of both the assets and liabilities involved. There is another important consideration: if you, as the heir, have debts of your own, your creditors could challenge your renunciation of a substantial inheritance on the grounds that you are doing so simply to avoid paying them.

Do you have further questions or need personalised advice? Get in touch with our family and succession law specialists, we are here to help you turn a difficult moment into a legally smooth transition.