.jpg)

How to Access Benefits for Self-Employed Workers?

Below is a summary overview of the key changes introduced by the new Royal Decree-Law 24/2020, of 26 June

SOCIAL SECURITY CONTRIBUTION EXEMPTIONS for Self-Employed Workers

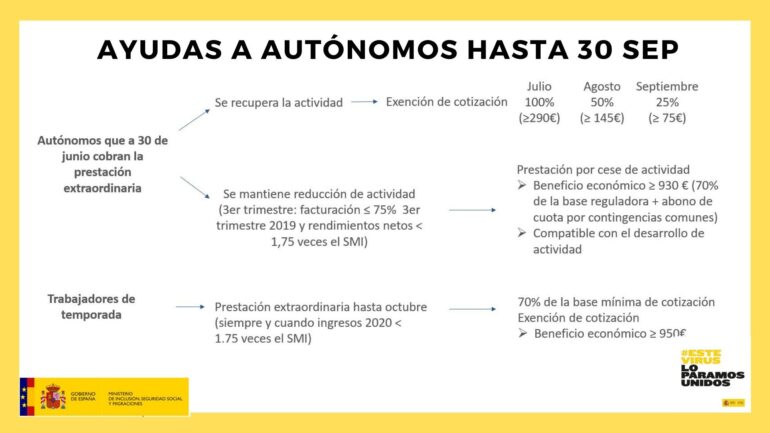

- From 1 July 2020, self-employed workers who were registered and were receiving the extraordinary cessation-of-activity benefit as at 30 June (the benefit under Article 17 of Royal Decree-Law 8/2020, of 17 March) will be entitled to an exemption from their Social Security and vocational training contributions at the following rates:

- 100% of contributions for July.

- 50% of contributions for August.

- 25% of contributions for September.

- There will also be an exemption from contributions during periods of temporary disability (IT) or other subsidies.

- There will be no contribution exemption if you are receiving the cessation-of-activity benefit.

The exemption will be applied automatically by the General Social Security Treasury for those self-employed workers who applied for the extraordinary benefit.

We have prepared a summary diagram for easier reference:

THE CESSATION-OF-ACTIVITY BENEFIT for self-employed workers:

- A employee self-employed worker who had been receiving the extraordinary cessation-of-activity benefit up to 30 June (under Article 17 of Royal Decree-Law 8/2020, of 17 March) may apply for the cessation-of-activity benefit provided for under former Article 327 of the General Social Security Act (LGSS), provided the following conditions are met:

Requirements:

- Be registered and active under the Special Scheme for Self-Employed Workers (RETA) or, where applicable, the Special Scheme for Sea Workers.

- Have completed the minimum contribution period for cessation-of-activity purposes referred to in Article 338.

- Not have reached the standard retirement age, unless the self-employed worker has not accrued the required contribution period for retirement.

- Be up to date with Social Security contributions (if this requirement is not met at the date of cessation of activity, the managing body will invite the self-employed worker to make payment within a non-extendable period of thirty calendar days. Regularising the arrears will produce full legal effect for the acquisition of the right to protection).

- Evidence a reduction in turnover (all 3 of the following conditions must be met):

- A 75% reduction in turnover during the third quarter of 2020 compared with the same period in 2019.

- Net income during the third quarter of 2020 must not have exceeded €5,818.75.

- Not having obtained MONTHLY net income exceeding €1,939.58.

At the time of applying for the benefit, self-employed workers with one or more employees must demonstrate compliance with all employment and Social Security obligations they have assumed. To do so, they must submit a statutory declaration, and may be required by the Social Security collaborating mutual societies or the managing body to provide the relevant supporting documents.

DURATION OF THE CESSATION OF ACTIVITY BENEFIT

This benefit may be received for a maximum period up to 30 September 2020.

It may be extended only if all the requirements set out in Article 330 of the aforementioned version of the General Social Security Act are met.

RECOGNITION OF THE BENEFIT:

On a provisional basis, recognition will be carried out by the collaborating mutual societies or the Social Institute of the Navy (Instituto Social de la Marina).

EFFECTS

The benefit takes effect from 1 July 2020 if applied for before 15 July, or from the day following the application in all other cases, and must be regularised from 31 January 2021.

OBLIGATIONS:

The self-employed employee, while receiving the benefit, must pay to the General Social Security Treasury (TGSS) the full amount of contributions calculated by applying the applicable rates to the corresponding contribution base.

For its part, the mutual society shall pay the employee, together with the cessation of activity benefit, the amount of common contingency contributions that would have been payable had the self-employed employee not been carrying out any activity, in accordance with the provisions of Art. 329 General Social Security Act (LGSS).

WAIVER OR REIMBURSEMENT:

There is the possibility of waiving or returning the benefit payment, subject to the following conditions:

- The benefit may be waived at any time before 31 August 2020, taking effect the month following notification.

- Reimbursement may be requested without waiting for a claim from the mutual society or the managing body, where the recipient considers that the income received during the third quarter of 2020, or the drop in turnover during that same period, will exceed the thresholds established for maintaining entitlement to the benefit.

Contact us if you need online or in-person assistance to apply for this benefit:

NEW EXTRAORDINARY CESSATION OF ACTIVITY BENEFIT FOR SEASONAL SELF-EMPLOYED WORKERS.

Seasonal self-employed workers are those whose only work over the previous two years was carried out:

- during the months of March to October (the summer season…)

- and who were registered as self-employed for at least five months per year during that period.

ELIGIBILITY REQUIREMENTS FOR THE BENEFIT:

- Having been registered and having made contributions under the Special Scheme for Self-Employed Workers (RETA) or the Special Scheme for Sea Workers as a self-employed employee for at least five months in the period between March and October, in each of the years 2018 and 2019.

- Not having been registered, or treated as registered, during the period from 1 March 2018 to 1 March 2020 under the applicable Social Security scheme as an employed employee for more than 120 days.

- Not having carried out any activity, nor having been registered or treated as registered, during the months of March to June 2020.

- Not having received any benefit from the Social Security system during the months of January to June 2020, unless that benefit was compatible with carrying out activity as a self-employed employee.

- Not having obtained income exceeding €23,275 during the year 2020.

- Being up to date with Social Security contributions. If this requirement is not met, the managing body will invite the self-employed employee to make payment within a non-extendable period of thirty calendar days. Regularising any outstanding contributions will take full effect for the purposes of acquiring entitlement to the benefit.

- Amount: The equivalent of 70% of the minimum contribution base applicable to the activity carried out under the Special Scheme for Self-Employed Workers or, where applicable, under the Special Scheme for Sea Workers.

- Accrual date of the extraordinary benefit: With effect from 1 June 2020.

- Duration: The maximum duration is 4 months, provided the application is submitted within the first fifteen calendar days of July. Otherwise, the benefit takes effect from the day following submission of the application.

- Benefit recognition: Applications may be submitted at any time during the period between the entry into force of the regulation and October 2020.

- No obligation to contribute: During the period in which the benefit is received, there is no obligation to make Social Security contributions. The employee remains registered, or in a status equivalent to registration, under the relevant Social Security scheme.

- Incompatibilities:

- This benefit is incompatible with employed work and with any Social Security benefit the recipient was already receiving, unless that benefit was compatible with carrying out work as a self-employed employee.

- It is likewise incompatible with self-employed work where income received during 2020 exceeds €23,275.

- Review: From 31 January 2021, all provisional decisions issued will be subject to review.

- Option to waive or repay the benefit:

- Waiver: At any time before 31 August 2020, with the waiver taking effect the month following notification.

- Repayment: On the recipient's own initiative, without waiting for a claim from the collaborating mutual insurance body or the managing entity, where the recipient considers that the income they may earn from their activity during the period in which entitlement could arise will exceed the thresholds set out in section 2(e), with the corresponding loss of entitlement to the benefit.

"Contact me if you need help applying for this new benefit. You can send me an email via my photo."

-1.png?width=111&name=circle-cropped%20(3)-1.png)